Is mortgage insurance required

Dylan Hughes

Published May 17, 2026

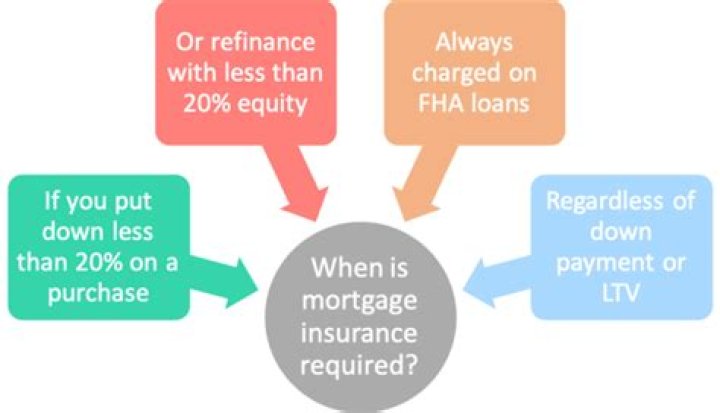

Typically, borrowers making a down payment of less than 20 percent of the purchase price of the home will need to pay for mortgage insurance. Mortgage insurance also is typically required on FHA and USDA loans. … But, it increases the cost of your loan.

Is it mandatory to have mortgage insurance?

Typically, borrowers making a down payment of less than 20 percent of the purchase price of the home will need to pay for mortgage insurance. Mortgage insurance also is typically required on FHA and USDA loans. … But, it increases the cost of your loan.

Does PMI ever go away?

This federal law, also known as the PMI Cancellation Act, protects you against excessive PMI charges. You have the right to get rid of PMI once you’ve built up the required amount of equity in your home.

Can you decline mortgage insurance?

But it’s not permanent. It drops off after five years due to increasing home value and decreasing loan principal. Remember, you can cancel mortgage insurance on a conventional loan when your mortgage balance falls to 80% of your home’s purchase price.Who pays the mortgage insurance?

Lender paid. There’s only one type of MIP, and the borrower always pays the premiums. But FHA loans don’t just have monthly MIPs. They also have an up-front mortgage insurance premium of 1.75% of the base loan amount.

Is it worth putting 20 down on a house?

The “20 percent down rule” is really a myth. Typically, mortgage lenders want you to put 20 percent down on a home purchase because it lowers their lending risk. It’s also a “rule” that most programs charge mortgage insurance if you put less than 20 percent down (though some loans avoid this).

Can FHA PMI be removed?

Getting rid of PMI is fairly straightforward: Once you accrue 20 percent equity in your home, either by making payments to reach that level or by increasing your home’s value, you can request to have PMI removed.

How can you avoid PMI without 20 down?

To sum up, when it comes to PMI, if you have less than 20% of the sales price or value of a home to use as a down payment, you have two basic options: Use a “stand-alone” first mortgage and pay PMI until the LTV of the mortgage reaches 78%, at which point the PMI can be eliminated. 1 Use a second mortgage.How much is PMI on a $100 000 mortgage?

While PMI is an initial added cost, it enables you to buy now and begin building equity versus waiting five to 10 years to build enough savings for a 20% down payment. While the amount you pay for PMI can vary, you can expect to pay approximately between $30 and $70 per month for every $100,000 borrowed.

Does PMI go towards principal?Private mortgage insurance does nothing for you This is a premium designed to protect the lender of the home loan, not you as a homeowner. Unlike the principal of your loan, your PMI payment doesn’t go into building equity in your home.

Article first time published onHow long do you pay mortgage insurance?

You pay the annual mortgage insurance premium, or MIP, in monthly installments for the life of the FHA loan if you put down less than 10%. If you put down over 10%, you pay MIP for 11 years. » MORE: Is an FHA loan right for you?

Why am I paying PMI on my mortgage?

Private mortgage insurance (PMI) is a type of insurance that conventional mortgage lenders require when homebuyers put down less than 20 percent of the home’s purchase price. PMI is designed to protect the lender in the event that the homeowner defaults on the loan.

Is FHA PMI permanent?

The good change is that FHA lowered its mortgage insurance premiums in January 2015. On the negative side, they’ve made PMI essentially permanent over the life of most mortgages that they insure.

How do I switch from FHA to conventional?

To convert an FHA loan to a conventional home loan, you will need to refinance your current mortgage. The FHA must approve the refinance, even though you are moving to a non-FHA-insured lender. The process is remarkably similar to a traditional refinance, although there are some additional considerations.

How much is PMI usually?

PMI typically costs 0.5 – 1% of your loan amount per year. Let’s take a second and put those numbers in perspective. If you buy a $300,000 home, you would be paying anywhere between $1,500 – $3,000 per year in mortgage insurance.

What are the disadvantages of a large down payment?

- Longer time to enter the market. The months or years spent saving for a large down payment can delay your readiness to buy a house. …

- Less short-term flexibility. …

- Interference with investments or retirement saving. …

- Benefits take a while to add up.

Is 25000 a good down payment?

You have $25,000 in savings to make a down payment, covering 10% of the home’s value. … Conventional wisdom might tell you to put down at least 20% of the home’s value, and that may be right for those with significant savings or an existing home to sell.

How much is a down payment on a 200k house?

Conventional mortgages, like the traditional 30-year fixed rate mortgage, usually require at least a 5% down payment. If you’re buying a home for $200,000, in this case, you’ll need $10,000 to secure a home loan. FHA Mortgage. For a government-backed mortgage like an FHA mortgage, the minimum down payment is 3.5%.

How can I avoid PMI with 5% down?

The traditional way to avoid paying PMI on a mortgage is to take out a piggyback loan. In that event, if you can only put up 5 percent down for your mortgage, you take out a second “piggyback” mortgage for 15 percent of the loan balance, and combine them for your 20 percent down payment.

Is PMI so bad?

Private Mortgage Insurance (PMI) Makes Low Down Payment Loans Possible. It’s an excellent time to be a home buyer with less than 20% down. … It’s important to realize, though, that mortgage insurance – of any kind – is neither “good” nor “bad”.

Is PMI based on credit score?

Credit scores and PMI rates are linked Insurers use your credit score, and other factors, to set that percentage. A borrower on the lowest end of the qualifying credit score range pays the most. “Typically, the mortgage insurance premium rate increases as a credit score decreases,” Guarino says.

Is PMI only for first time buyers?

But if you don’t have the full 20% down payment, your lender will probably want a little extra insurance that you’ll pay your loan as agreed. … But here’s a secret: Not all first-time buyers have to pay PMI or MI.

Can I avoid PMI with 10 percent down?

Get an 80-10-10 loan One loan covers 80% of the home price, and the other loan covers a 10% down payment. Combined with your savings for a 10% down payment, this type of loan can help you avoid PMI.

Does mortgage insurance go away after 20 percent?

Once you build up at least 20 percent equity in your home, you can ask your lender to cancel this insurance. And your lender must automatically cancel PMI charges once your regular payments reduce the balance on your loan to 78 percent of your home’s original appraised value.

How can you avoid PMI?

One way to avoid paying PMI is to make a down payment that is equal to at least one-fifth of the purchase price of the home; in mortgage-speak, the mortgage’s loan-to-value (LTV) ratio is 80%. If your new home costs $180,000, for example, you would need to put down at least $36,000 to avoid paying PMI.

How long do I have to pay PMI on a FHA loan?

Mortgage insurance (PMI) is removed from conventional mortgages once the loan reaches 78 percent loan–to–value ratio. But removing FHA mortgage insurance is a different story. Depending on your down payment, and when you first took out the loan, FHA MIP usually lasts 11 years or the life of the loan.

Does FHA require homeowners insurance?

All FHA loans require borrowers to pay mortgage insurance premiums (MIP). The mortgage insurance protects the lender in the event that a borrower defaults on their mortgage.

Is Conventional better than FHA?

FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.

Do conventional loans require PMI?

If you put down less than 20% on a conventional loan, you’ll be required to pay for private mortgage insurance (PMI). PMI protects your lender in case you default on your loan. The cost for PMI varies based on your loan type, your credit score and the size of your down payment.

What is the minimum credit score for a conventional loan?

Conventional Loans A conventional loan is a mortgage that’s not insured by a government agency. Most conventional loans are backed by mortgage companies Fannie Mae and Freddie Mac. Fannie Mae says that conventional loans typically require a minimum credit score of 620.