How much bad debt can I write off

Andrew Vasquez

Published May 27, 2026

It’s a short-term capital loss, so you must first deduct it from any short-term capital gains you have before deducting it from long-term capital gains. Finally, you can deduct up to $3,000 of any remaining balance from other income. If a balance still remains, you can carry it over to subsequent years.

What debt is tax deductible?

The interest you pay on consumer debt falls into two distinct categories: tax-deductible and nondeductible. Mortgage interest is generally tax-deductible. So is interest paid on student loans and money borrowed to buy investment property, including stocks, bonds and mutual funds, up to certain limits.

How is bad debt treated for tax purposes?

A business deducts its bad debts, in full or in part, from gross income when figuring its taxable income. … Nonbusiness bad debts must be totally worthless to be deductible. You can’t deduct a partially worthless nonbusiness bad debt.

What happens when you write off a bad debt?

When debts are written off, they are removed as assets from the balance sheet because the company does not expect to recover payment. In contrast, when a bad debt is written down, some of the bad debt value remains as an asset because the company expects to recover it.What are examples of bad debt?

- Credit Card Debt. Owing money on your credit card is one of the most common types of bad debt. …

- Auto Loans. Buying a car might seem like a worthwhile purchase, but auto loans are considered bad debt. …

- Personal Loans. …

- Payday Loans. …

- Loan Shark Deals.

How can I legally not pay taxes?

- Contribute significant amounts to retirement savings plans.

- Participate in employer sponsored savings accounts for child care and healthcare.

- Pay attention to tax credits like the child tax credit and the retirement savings contributions credit.

- Tax-loss harvest investments.

Can I write off all my debts?

Also , creditors may agree to write off part of a debt, or in some cases all of it, but this depends on your situation. … You may be able to apply for a debt solution that will write off some or all your debts, if it’s unlikely you’ll be able to pay what you owe in a reasonable amount of time.

Is a car payment considered debt?

The auto loan itself would be considered the “debt.” The payments toward it would be considered “debt payments.” With regard to your credit report, if you are applying for another loan somewhere and they looked at your debt-to-income ratio, the monthly auto loan payments would be included on the debt side.When Should bad debt be written off?

The general rule is to write off a bad debt when you’re unable to contact the client, they haven’t shown any willingness to set up a payment plan, and the debt has been unpaid for more than 90 days.

Is a car payment bad debt?Some auto loans may carry a high interest rate, depending on factors including your credit scores and the type and amount of the loan. However, an auto loan can also be good debt, as owning a car can put you in a better position to get or keep a job, which results in earning potential.

Article first time published onHow do you know the difference between a good debt and a bad debt?

Good debt has the potential to increase your net worth or enhance your life in an important way. Bad debt involves borrowing money to purchase rapidly depreciating assets or only for the purpose of consumption.

Is a debt written off after 6 years?

For most debts, if you’re liable your creditor has to take action against you within a certain time limit. … For most debts, the time limit is 6 years since you last wrote to them or made a payment. The time limit is longer for mortgage debts.

How do I ask for debt forgiveness?

- Save in advance. …

- Find out who owns the debt. …

- Make a call. …

- Ask if the creditor or collection agency will settle for less and forgive part of your debt. …

- Get the offer in writing.

Is there a government debt relief program?

There is no government program that forgives or even minimizes the burden of paying off your credit card balances. There are, however, 501(c)3 nonprofit consumer credit counseling services that work with you to provide debt relief. These agencies are funded through grants from credit card companies.

How do millionaires avoid taxes?

While most Americans earn money through labor, such as salaries and benefits, the super affluent may receive income from interest, dividends, capital gains or rent, from investments, known as capital income. … The affluent often hold assets until death, avoiding capital gains taxes by passing property to heirs.

How can a single person save on taxes?

- Deduct expenses even if you don’t itemize. …

- Deduct interest paid by mom and dad. …

- Time your wedding. …

- Marry your withholding, too. …

- Roll over an inherited 401(k). …

- Check the calendar before you sell. …

- Don’t buy a tax bill. …

- Make your IRA contributions sooner rather than later.

How do I settle myself with the IRS?

You have two options to file an Offer in Compromise. You can work with a tax debt resolution service or you can try to file on your own. If you want to settle tax debt yourself, simply download the IRS Form 656 Booklet. In includes Form 656 and Form 433-A form that you need to fill out for your financial disclosure.

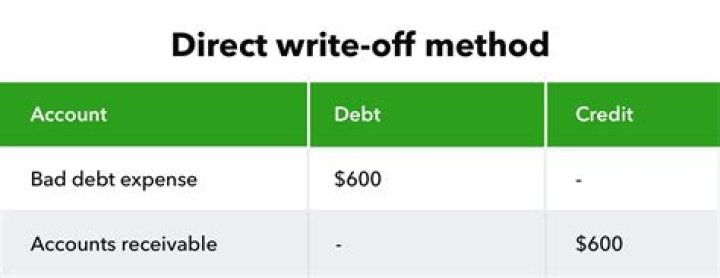

What is the difference between bad debts and bad debts written off?

A bad-debt expense anticipates future losses, while a write-off is a bookkeeping maneuver that simply acknowledges that a loss has occurred.

What are the three C's of credit?

Character, Capacity and Capital.

Is debt a bad thing?

Too much debt can turn good debt into bad debt. You can borrow too much for important goals like college, a home, or a car. Too much debt, even if it is at a low interest rate, can become bad debt. Carrying debt without a good plan to pay it off can lead to an unsustainable lifestyle.

What is a major risk of debt?

A key risk of borrowing now and leveraging future cash flow is that sales could slump at some point, making it difficult to make payments. This can lead to missed payments, late fees and negative hits on your credit score. … Thus, if you fail to keep up with payments, you risk property seizure by the bank.

Why you should never have a car payment?

Most people get a ton of car debt, which makes it so much harder to really invest. When you increase your debts, you spend more of your monthly income paying those debts, and save less money each money for investments. On top of it, every loan you have puts you further away from buying a home or investment property.

What is considered a high car payment?

According to experts, a car payment is too high if the car payment is more than 30% of your total income. Remember, the car payment isn’t your only car expense! Make sure to consider fuel and maintenance expenses. Make sure your car payment does not exceed 15%-20% of your total income.

What is a reasonable car payment?

To cut to the chase, it’s smart to spend less than 10% of your monthly take-home pay on your car payment, so you can keep your total car costs below 15% to 20% of your income. That might leave you feeling you can afford only a beat-up Yugo. But there’s an interesting caveat to this rule of thumb.

What types of debt should be avoided?

- Credit Card Debt. With credit cards promising a luxury and care free lifestyle at the tap of your fingers – it’s no surprise that many people have spiralled into a credit card debt cycle. …

- Student Loan Debt. …

- Medical Debt. …

- Car Loan Debt.

What is considered personal debt?

Definition. Personal debt is debt owed for which you personally are legally responsible. … Secured debt is debt acquired by putting up some form of collateral. Unsecured debt relies solely on your promise to pay. Personal debt always funds consumption rather than investment.

How long before a debt becomes uncollectible?

In California, the statute of limitations for consumer debt is four years. This means a creditor can’t prevail in court after four years have passed, making the debt essentially uncollectable.

Is it true that after 7 years your credit is clear?

Even though debts still exist after seven years, having them fall off your credit report can be beneficial to your credit score. … Note that only negative information disappears from your credit report after seven years. Open positive accounts will stay on your credit report indefinitely.

Can debt be written off after 5 years?

Can Old Debts be Written Off? Well, yes and no. After a period of six years after you miss a payment, the default is removed from your credit file and no longer acts negatively against you. … This means that (with the exception of Council Tax bills), the creditor cannot use legal means to enforce you to pay a debt.

Is forgiveness of debt taxable?

In general, if you have cancellation of debt income because your debt is canceled, forgiven, or discharged for less than the amount you must pay, the amount of the canceled debt is taxable and you must report the canceled debt on your tax return for the year the cancellation occurs.

Can I ask a bank to forgive debt?

In some cases, banks will forgive the borrower the difference in a transaction called a short-sale. If you have experienced serious financial issues, you can also attempt to ask other debtors for forgiveness such as credit cards, personal loans and car loans.