How do you write off a dead stock

Eleanor Gray

Published Apr 25, 2026

Obsolete inventory is inventory at the end of its product life cycle that needs to be either written-down or written-off the company’s books. Obsolete inventory is written-down by debiting expenses and crediting a contra asset account, such as allowance for obsolete inventory.

How do you record a loss of inventory?

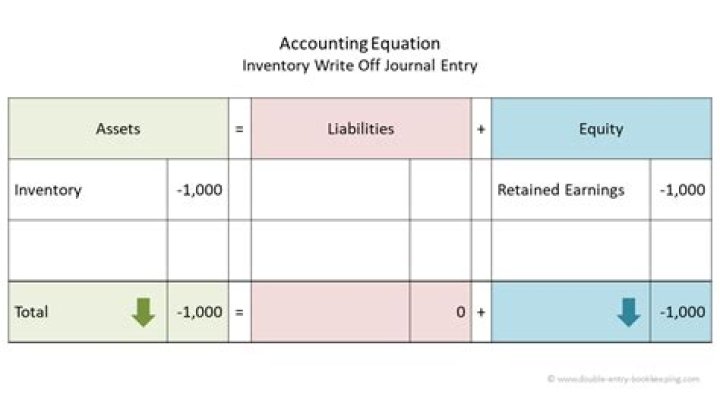

Losses are entered in the inventory asset account as a credit. A debit entry must be made in an expense account; it’s called a write-down of inventory account or loss of inventory account.

Which of the three reasons of why inventory might have to be written off?

- Inventory is stolen. Unfortunately, small and large inventory have a tendency to disappear. …

- Inventory has been damaged at any part of the supply chain. …

- Inventory isn’t relevant to the market anymore. …

- Inventory was perishable.

When can you write off inventory?

Writing off inventory involves removing the cost of no-value inventory items from the accounting records. Inventory should be written off when it becomes obsolete or its market price has fallen to a level below the cost at which it is currently recorded in the accounting records.Can you sell written off inventory?

There is no rule that says a company can’t later use or sell inventory that has been written off. … A company generally cannot take a current tax deduction for inventory that has been written off if it’s still on hand.

Can you write up inventory?

When inventory loses partial value, it must be recorded as an inventory write-down expense on a company’s balance sheet, and it must be made as soon as possible to lessen tax liability.

Can I write-off obsolete inventory?

Can I write off expired inventory? Expired inventory can be written off as if it were lost or damaged because it has lost its market value and can no longer be used for its normal intended purposes.

What is the difference between write-down and write-off?

A write-down reduces the value of an asset for tax and accounting purposes, but the asset still remains some value. A write-off negates all present and future value of an asset. It reduces its value to zero.How do I write-off damaged inventory in Quickbooks?

- Go to Banking.

- Click Make Deposit.

- Choose a customer and enter necessary information.

- Use your Miscellaneous Income account in the From Account column on the deposit screen.

- Click Save & Close.

In regards to GAAP, once you have identified inventory that you cannot sell, you must write this inventory off as an expense. Assuming no receipt of payment for the inventory, you will debit a cost of goods sold account and credit either inventory directly or your inventory reserve account.

Article first time published onHow can I reduce my write offs?

- Avoid Excess Purchasing. …

- Create an Inventory Reserve. …

- Utilize Write-Downs as Needed. …

- Revise the Order Cycle Regularly. …

- Eliminate Obsolete Stock.

How do I write off bad debt?

Under the direct write-off method, bad debts are expensed. The company credits the accounts receivable account on the balance sheet and debits the bad debt expense account on the income statement. Under this form of accounting, there is no “Allowance for Doubtful Accounts” section on the balance sheet.

Can you write up inventory under IFRS?

IFRS requires that inventory is carried at the lower of cost or net realizable value; U.S. GAAP requires that inventory is carried at the lower of cost or market value. IFRS allows for some inventory reversal write-downs; GAAP does not.

Is goodwill ever written up?

Goodwill is acquired and recorded on the books when an entity purchases another entity for more than the fair market value of its assets. … In some cases, goodwill may be completely written off and removed from the balance sheet.

What is reversal of inventory write down?

Reversal of Inventory Write Down For example, this happens when the initial write-down estimated loss is higher than the net realizable value of the inventory. An assessment is done during each reporting period and, if there is clear evidence of a value difference, then a reversal of inventory write-down is executed.

How do I write-off a bad debt in QuickBooks?

- Step 1: Check your aging accounts receivable. …

- Step 2: Create a bad debts expense account. …

- Step 3: Create a bad debt item. …

- Step 4: Create a credit memo for the bad debt. …

- Step 5: Apply the credit memo to the invoice. …

- Step 6: Run a bad debts report.

Are damaged goods included in inventory?

If you occasionally write off small amounts of damaged inventory, you do not have to make a separate disclosure on the income statement. The loss is included in with the cost-of-goods-sold amount. … A separate account such as loss from write-off of Inventory is included with the other inventory accounts.

What qualifies as a write-off?

A write-off is a business expense that is deducted for tax purposes. … The cost of these items is deducted from revenue in order to decrease the total taxable revenue. Examples of write-offs include vehicle expenses and rent or mortgage payments, according to the IRS.

What technical write-off?

A technical write-off is made when the bank removes an account from the NPA category even as it continues to make efforts to recover the amount involved. The other kind is when the bank takes the loan off its books altogether while providing fully for it.

How does a write-off work?

A tax deduction (or “tax write-off”) is an expense that you can deduct from your taxable income. You take the amount of the expense and subtract that from your taxable income. Essentially, tax write-offs allow you to pay a smaller tax bill.

Do write offs affect assets?

When a business takes a write-off, it is a deduction in the value of earnings by the amount of an expense or loss. … If the account becomes uncollectible, it means that the business no longer considers it an asset and it must record that in its financial statements for transparency to investors.

Can you write-off your car?

Individuals who own a business or are self-employed and use their vehicle for business may deduct car expenses on their tax return. If a taxpayer uses the car for both business and personal purposes, the expenses must be split. The deduction is based on the portion of mileage used for business.

How do you write-off cost of goods sold?

Here you provide the cost of all merchandise you purchased during the year. If you manufactured goods for sale, include the costs of all raw materials you purchased in the year that were necessary to manufacture those goods. Subtract the cost of any items withdrawn for personal use.

When can I write off a bad debt?

It is necessary to write off a bad debt when the related customer invoice is considered to be uncollectible. Otherwise, a business will carry an inordinately high accounts receivable balance that overstates the amount of outstanding customer invoices that will eventually be converted into cash.

What methods have you used for estimating bad debt?

- Percentage of Sales. Percentage of sales involves determining what percentage of net credit sales or total credit sales is uncollectible. …

- Percentage of Receivables.

How are bad debts treated in accounting?

Bad debt expenses are generally classified as a sales and general administrative expense and are found on the income statement. Recognizing bad debts leads to an offsetting reduction to accounts receivable on the balance sheet—though businesses retain the right to collect funds should the circumstances change.

How do you value inventory under GAAP?

Under US GAAP, inventories are measured at the lower of cost, market value, or net realisable value depending upon the inventory method used. Market value is defined as current replacement cost subject to an upper limit of net realizable value and a lower limit of net realizable value less a normal profit margin.

Can you reverse inventory reserve?

The establishment of a reserve for excess and obsolete inventory establishes a new cost basis in the inventory. Such reserves are not reduced until the product is sold. If we are able to sell such inventory any related reserves would be reversed in the period of sale.”

What costs are included in inventory?

The cost of inventory includes the cost of purchased merchandise, less discounts that are taken, plus any duties and transportation costs paid by the purchaser.